Lessons from Hurricane Sandy about Annuities

Where does an annuity fit in your retirement portfolio?

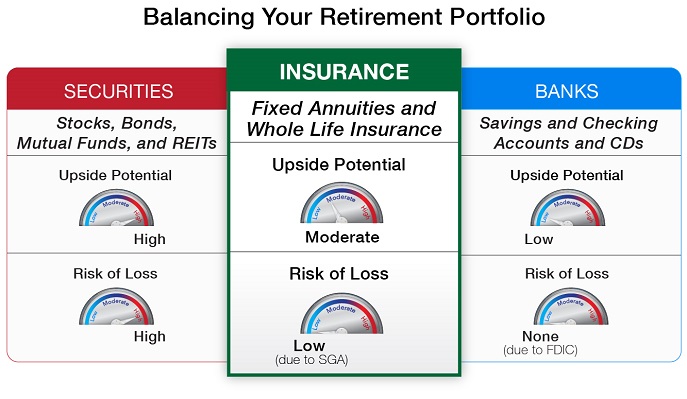

One of the best ways I have to explain the role of annuities in your retirement portfolio is to show you how each of the three main financial services sectors addresses planning for your retirement:

1. The first group is the Securities industry. This group gives you products like stocks, bonds, and mutual funds.

2. The second group is the Insurance industry. This group sources actuarial and risk products like guaranteed annuities.

3. The third group is the Banking industry. This group is the perennial source of certificates of deposit and savings and checking accounts.

Let’s consider the general pros and cons of each group from two important general aspects: upside growth potential for your money and the risk of loss to your money.

We’ll start with securities. Securities offer the best upside growth potential, depending on the specific financial vehicles. On the other hand, you may dislike the moderate to high risk of loss to your money that comes with securities.

I bought two annuities this year and was extremely satisfied with the service from Immediate Annuities.com each time. In short, their staff was courteous, professional, and prompt. I would recommend them to anyone who wants to buy an annuity.

Now, let’s look at the banks. The banking sector feels safe due to the lack of risk to your money. Your risk of loss with FDIC coverage is virtually nil when your money is in a CD or a savings account. Unfortunately, any real upside growth potential is also very low.

Then there's the insurance industry. Guaranteed annuities sit in between securities and savings accounts. They offer moderate upside growth potential for your money with SGA protection. The growth potential is lower than securities, but generally much higher than with banks. What's more, with annuities, your growth potential, or interest earnings, can be guaranteed.

You are right to consider an annuity part investment, because you give a sum of money to a financial institution with the hope that you’ll get back more than you put in; and also, insurance, because a small portion of your premium buys a guarantee (the exact nature of the guarantee varies with the type of annuity).

For example: With a multi-year or index annuity contract, your guarantee is the rate of interest earned for a certain number of years. With an immediate annuity, your guarantee is the promise of dependable monthly income.

So an annuity is all about the trade-off between risk and reward. The guarantees reduce your risk of losing money, but the cost of the guarantees reduces your potential return. In other words, by lowering your risk you also lower your potential reward.

If anybody tries to convince you otherwise, put your hand on your wallet and slowly back away. There are no free lunches. (Beware of index or hybrid annuities that promise the world.)

To sum up, the biggest reasons to include an annuity in your retirement portfolio is safety and balance. An annuity offers you the middle path between the extreme risk and reward offered by securities and the extremely low upside potential offered by banks. And it offers you safety and protection against loss.

If this appeals to you, then an annuity may have a place in your retirement portfolio.

We'd love to hear from you!

Please post your comment or question. It's completely safe – we never publish your email address.

Comments (0)

There are no comments yet. Do you have any questions?