Annuity Trends — Learn What Drives Annuity Payout Rates

Are annuity rates going up or down? The truth is, we often don’t know for certain. Insurance companies sometimes announce rate changes a week or so in advance—but they don’t always do that.

The good news: with over thirty years experience tracking annuity rates, we have extensive data showing what drives annuity rates. In this article, we will:

- Explain what insurance companies invest in

- Examine how those investments impact annuity rates

- Show you charts illustrating the relationships between investments and annuity rates

Understanding these factors can help you make informed, confident decisions when buying an annuity.

Where Are Annuity Rates Right Now?

Because annuity payouts vary by age, gender, and annuity type, the most reliable way to see what an income annuity would pay you is to run a quote using our blue annuity calculator on this page.

You’ll get instant annuity rates online from top-rated providers like New York Life, MassMutual, Guardian, Nationwide and more. It’s fast, free, and easy — and best of all, no phone number is required to see your personalized annuity quote.

How Do Insurers Set Their Annuity Rates?

Understanding how insurers are investing their money is key to understanding how they set annuity rates.

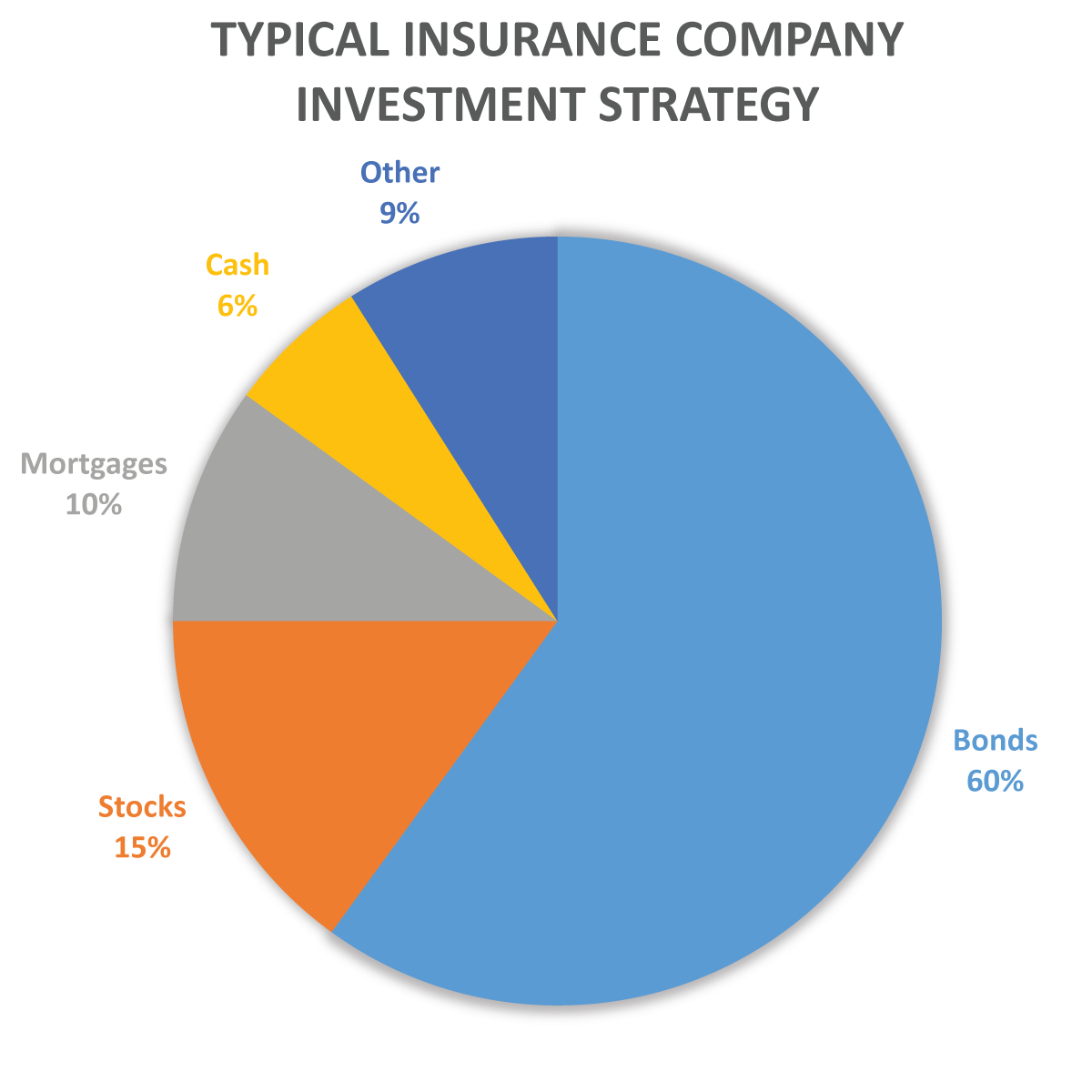

A typical insurance company’s investment portfolio looks something like this:

- Bonds: ~60%

- Stocks: ~15% or less

- Mortgages: ~10%

- Cash: ~6%

- Other investments: ~ 9%

As you can see, insurers invest heavily in bonds. The yields they earn on these bonds play a major role in determining annuity payout rates.

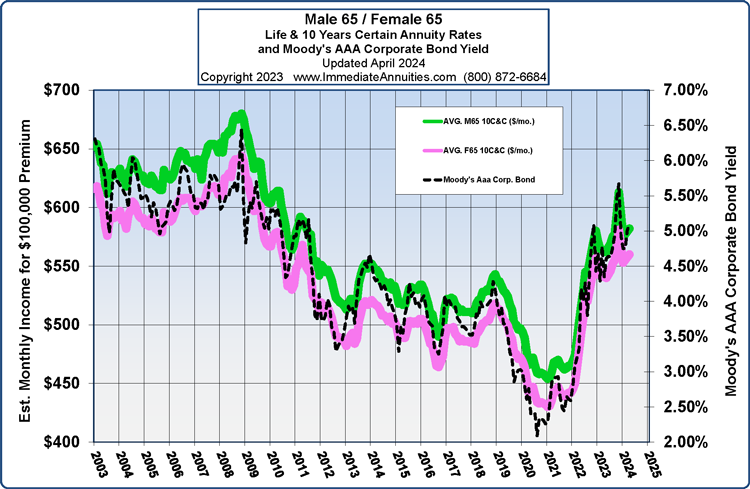

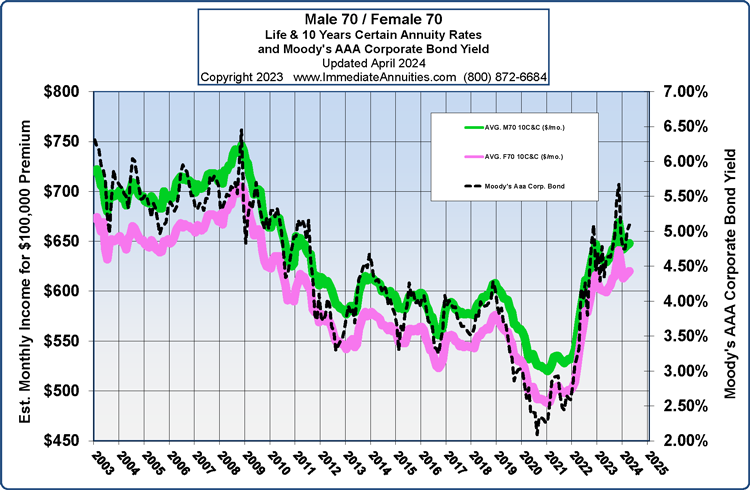

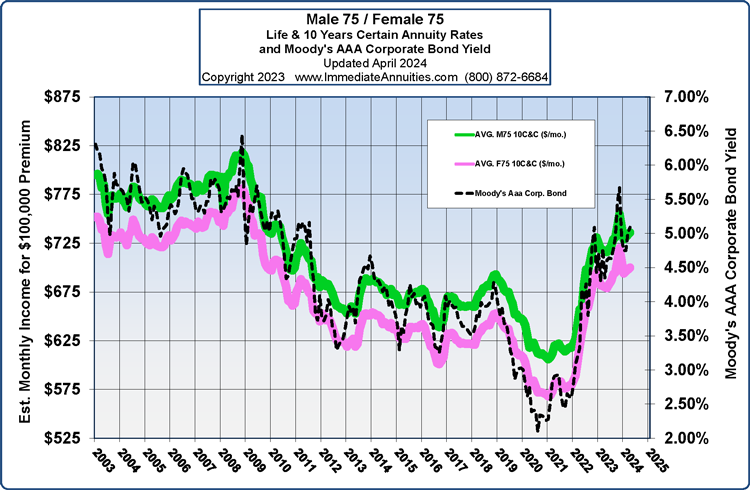

We track Moody’s Aaa Corporate Bond index (DAAA), which consists of highly rated, long-term bonds with maturities of 20 years or more. Historically, there is a strong relationship between this bond index and annuity rates, making it a useful way to understand how insurers determine annuity payouts.

What Makes Annuity Rates Go Up and Down?

As we’ve seen, insurers rely on bonds to back their annuity payouts. Because of this, changes in bond rates play a major role in determining annuity payout rates.

The charts below illustrate the historical relationship between Moody’s Aaa Corporate Bond rates and payouts for a Life with 10 Years Certain immediate annuity. You’ll notice that when bond rates rise or fall, annuity payouts tend to follow suit.

Should You Try To Time When To Buy Your Annuity?

Can you time when to buy your annuity using bond market trends? This is extremely difficult. You would need to predict both bond market movements and how insurers adjust their rates—something even experts cannot do reliably.

Another thing people try to do is use predicted moves in the Federal Reserve Rate to time their annuity purchase. You can also check out our article on if the Fed rate impacts annuity rates to learn why this is also not a surefire way to get more income.

Timing the market is notoriously hard, and getting it wrong can leave you worse off for trying. Instead, many people use strategies like an annuity ladder to hedge against buying during a period of low rates.

Ultimately, some of the best advice financial professionals give is: buy the annuity when you need the income.

Have Questions About Annuity Trends?

If you still have questions about annuity trends or want to speak with an annuity expert about your plans, just call us at (866) 866-1999. We promise to give you honest answers to your questions without any sales pressures. We’re here to help.

What makes annuity rates go up or down?

Since insurers invest a large portion of their portfolios in bonds, how bond rates move have a strong impact on annuity rates. When bond rates go up, annuity payout rates tend to follow along.

How does a life insurance company invest my money?

Most life insurance companies invest 60% or so of their portfolios into fixed income vehicles like bonds. They also typically invest less than 15% in common stocks. This portfolio composition gives them the stability to provide benefits to their customers in both good and bad markets.

Can I time my annuity purchase?

This is very hard to do. If you get it wrong, you may be worse off for trying. When you wait to buy your annuity, you are giving up income while you wait (opportunity cost) with no guarantee that rates will rise. Many people use an annuity ladder to ease into an annuity purchase instead of trying to time the markets.

How do insurance companies set their annuity rates?

Insurance companies typically invest the majority of their capital in bonds, providing them with fixed returns. They set their rates by determining what they expect to earn on their bond holdings and issuing an annuity based on these returns. As a result, when bond rates are better, annuity rates also tend to improve.