With Interest Rates The Way They Are, Should I Wait To Buy My Annuity?

Timing when to start your annuity can be stressful. This is especially true if you are hoping to predict future annuity rates. To add to the confusion, you may keep hearing about the “Fed” changing interest rates. While we can't know the future of annuity rates, here are some insights to help your decision.

What Rates Should You Follow?

To understand why annuity rates change, let's consider how insurance companies invest. An insurer wants an investment that is going to be stable over a long period of time. After all, they are investing to cover the golden years of many retirees. For some people this could be 30 years or longer!

To do this, insurance companies invest a large percentage of their assets in high-quality bonds. They choose these types of investments for their predictable stability. Since annuities are long-term contracts, their payouts correlate with long-term rates. As a result, annuity rates closely follow bonds with a duration of 20 or more years.

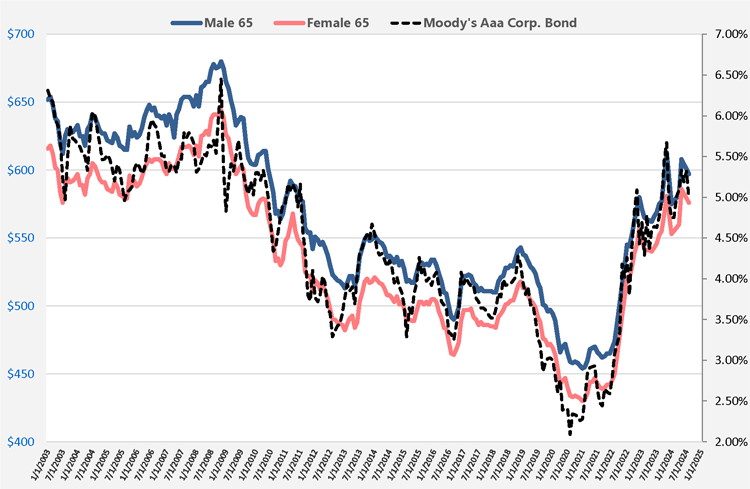

The chart below shows payout rates for Life with 10 Years Certain annuities and Moody’s Aaa Corporate Bonds with maturities of 20 years and longer.

Single Life With 10 Years Certain Annuity Payouts and Moody's Aaa Corporate Bond Rates

What About The "Fed Rate"

You may hear about the Fed declaring rate changes and wonder if it will affect annuity payouts. The short answer is: not necessarily. Annuity rates aren’t directly affected by the Fed Rate. That’s because annuity rates reflect long-term rates, and the Fed rate is a short-term rate.

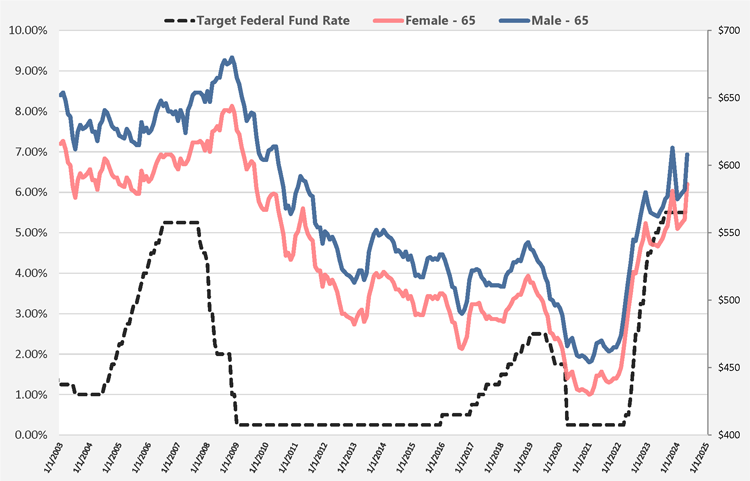

This doesn’t mean there isn’t any relationship between the two. The Fed Rate isn’t a strong indicator of imminent changes in annuity rates, but it may have a general effect on bond rates. Take a look at the chart below showing the Target Federal Fund Rate and Average Annuity Rates. There’s a lot more variance in the Fed Rate. So you may be surprised when annuity rates don't move in lock-step with Fed Rate changes.

To illustrate this, below we have a graph of the Target Federal Fund Rate and Single Life With 10 Years Certain Annuity Payouts.

Effective Federal Fund Rate, Short-Term 1 Year Bond Rates, And Long-Term Moody's Aaa Corp. Bond Rates

Live Long and Prosper

With a lifetime annuity, how long you live affects how much money you make. This is a key point to understand. If you wait a year for rates to increase, that’s one less year of income you earn.For waiting to make sense, increases in your payout rate need to make up for this lost income. Let’s consider a hypothetical situation.

Frank is 65 years old and wants to buy a $100,000 Single Life with Cash Refund Immediate Annuity. As of August 2019, he would get about $517 each month. But what if he were one year older, rates went up by a little over 5%, and he was getting $543 per month? He would be getting $26 more per month! But Frank would have also missed out on $6,204 of payments while he waited for rate increases.

To make up for lost income, Frank would have to live at least 20.9 years. We calculate this by dividing $6,204 by $26, and then convert those 238 months into 19.9 years. But then we also need on the year Frank didn't get income. We wish Frank a long life, but according to the CSO Mortality Table his life expectancy is only 16.80 years.

Hypothetical Accumulated Income Comparison of Waiting One Year to Begin Income Frank's Life Expectancy: 16.80 years Time To Recover Income: 20.90 years

| Contract Year | Age In Years | $517 Per Month $6,204 Annually |

$543 Per Month $6,514 Annually |

|---|---|---|---|

| 1 | 65 | $6,204 | $– |

| 2 | 66 | $12,408 | $6,514 |

| 3 | 67 | $18,612 | $13,208 |

| 4 | 68 | $24,816 | $19,543 |

| 5 | 69 | $31,020 | $26,057 |

| 6 | 70 | $37,224 | $32,571 |

| 7 | 71 | $43,428 | $39,085 |

| 8 | 72 | $49,632 | $45,599 |

| 9 | 73 | $55,836 | $52,114 |

| 10 | 74 | $62,040 | $58,628 |

| 11 | 75 | $68,244 | $65,142 |

| 12 | 76 | $74,448 | $71,656 |

| 13 | 77 | $80,652 | $78,170 |

| 14 | 78 | $86,856 | $84,685 |

| 15 | 79 | $93,060 | $91,199 |

| 16 | 80 | $99,264 | $97,713 |

| 17 | 81 | $105,468 | $104,227 |

| 18 | 82 | $111,672 | $110,741 |

| 19 | 83 | $117,876 | $117,256 |

| 20 | 84 | $124,080 | $123,770 |

| 21 | 85 | $130,284 | $130,284 |

| 22 | 86 | $142,692 | $143,312 |

| All values are hypothetical and for informational purposes only. For current quotes and rates, visit www.ImmediateAnnuities.com. This chart is not intended to be a recommendation to purshase an annuity. | |||

This doesn't mean that waiting is always a bad idea. The uncertainty of future annuity rates and how long you will live means there is no 'right' or 'wrong' choice. And, there are strategies to protect you from locking in a low rate while not missing out on earning income. You can read about one of these strategies, annuity laddering, or call one of our experts at 800-872-6684. We’re happy to help you plan your annuity purchase.

We'd love to hear from you!

Please post your comment or question. It's completely safe – we never publish your email address.

Comments (4)

Pat D.

2022-10-08 00:46:33

In my case waiting for a 4.75-5.25% RoR on an immediate 15 yr certain annuity is not going to hurt total return, because it's certain to go to my beneficiary, I'm earning 3% in the savings account the premium is stored in and I plan on gifting the exclusion portion of the monthly checks to my sister. I have been retired 11 yrs and have multiple income streams, so the potential new annuity is a bonus, not a necessity.

Z. M.

2023-05-30 20:01:25

Well in my case waiting for a 4.75-5.25% RoR on an immediate 15 yr certain annuity is not going to hurt total return, because it's certain to go to my beneficiary, I'm earning 3% in the savings account the premium is stored in and I plan on gifting the exclusion portion of the monthly checks to my brother. I have been retired 10 yrs and have multiple income streams, so the potential new annuity is a bonus, not a necessity.

Eldon

2023-11-15 11:01:43

If I take out a QLAC, do I still pay RMD.

Kyle

2023-11-16 13:03:00

Hi Eldon,

Thank you for reaching out.

If you take out a QLAC, you'll still need to pay RMDs on any remaining IRAs that you have outside of the QLAC.

Best regards,

Kyle